备注

Go to the end 下载完整的示例代码。或者通过浏览器中的MysterLite或Binder运行此示例

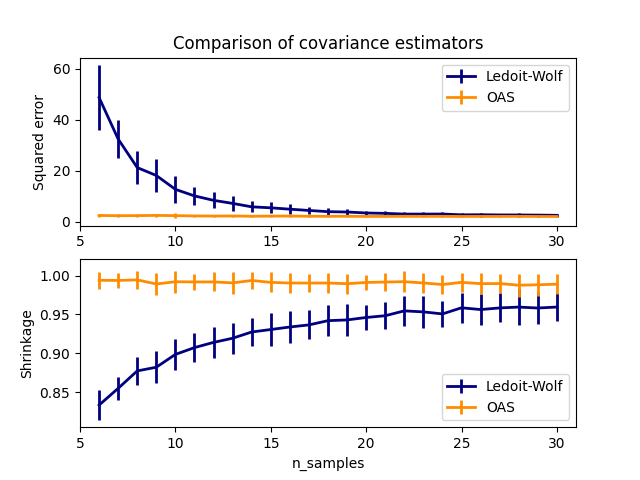

Ledoit-Wolf与OAS估计#

通常的协方差最大似然估计可以使用收缩进行正规化。Ledoit-Wolf提出了一个封闭的公式来计算渐进最优收缩参数(最小化SSE标准),从而产生Ledoit-Wolf协方差估计。

Chen等人提出了对Ledoit-Wolf收缩参数OAS系数的改进,在假设数据为高斯的情况下,其收敛性明显更好。

这个例子,灵感来自陈的出版物 [1] ,显示了使用高斯分布数据对LW和OAS方法估计的SSE进行比较。

[1] “用于MMSE协方差估计的收缩算法”Chen等人,IEEE Trans. on Sign。程序。,第58卷,第10期,2010年10月。

# Authors: The scikit-learn developers

# SPDX-License-Identifier: BSD-3-Clause

import matplotlib.pyplot as plt

import numpy as np

from scipy.linalg import cholesky, toeplitz

from sklearn.covariance import OAS, LedoitWolf

np.random.seed(0)

n_features = 100

# simulation covariance matrix (AR(1) process)

r = 0.1

real_cov = toeplitz(r ** np.arange(n_features))

coloring_matrix = cholesky(real_cov)

n_samples_range = np.arange(6, 31, 1)

repeat = 100

lw_mse = np.zeros((n_samples_range.size, repeat))

oa_mse = np.zeros((n_samples_range.size, repeat))

lw_shrinkage = np.zeros((n_samples_range.size, repeat))

oa_shrinkage = np.zeros((n_samples_range.size, repeat))

for i, n_samples in enumerate(n_samples_range):

for j in range(repeat):

X = np.dot(np.random.normal(size=(n_samples, n_features)), coloring_matrix.T)

lw = LedoitWolf(store_precision=False, assume_centered=True)

lw.fit(X)

lw_mse[i, j] = lw.error_norm(real_cov, scaling=False)

lw_shrinkage[i, j] = lw.shrinkage_

oa = OAS(store_precision=False, assume_centered=True)

oa.fit(X)

oa_mse[i, j] = oa.error_norm(real_cov, scaling=False)

oa_shrinkage[i, j] = oa.shrinkage_

# plot MSE

plt.subplot(2, 1, 1)

plt.errorbar(

n_samples_range,

lw_mse.mean(1),

yerr=lw_mse.std(1),

label="Ledoit-Wolf",

color="navy",

lw=2,

)

plt.errorbar(

n_samples_range,

oa_mse.mean(1),

yerr=oa_mse.std(1),

label="OAS",

color="darkorange",

lw=2,

)

plt.ylabel("Squared error")

plt.legend(loc="upper right")

plt.title("Comparison of covariance estimators")

plt.xlim(5, 31)

# plot shrinkage coefficient

plt.subplot(2, 1, 2)

plt.errorbar(

n_samples_range,

lw_shrinkage.mean(1),

yerr=lw_shrinkage.std(1),

label="Ledoit-Wolf",

color="navy",

lw=2,

)

plt.errorbar(

n_samples_range,

oa_shrinkage.mean(1),

yerr=oa_shrinkage.std(1),

label="OAS",

color="darkorange",

lw=2,

)

plt.xlabel("n_samples")

plt.ylabel("Shrinkage")

plt.legend(loc="lower right")

plt.ylim(plt.ylim()[0], 1.0 + (plt.ylim()[1] - plt.ylim()[0]) / 10.0)

plt.xlim(5, 31)

plt.show()

Total running time of the script: (0分2.118秒)

相关实例

收缩协方差估计:LedoitWolf vs OAS和最大似然

Shrinkage covariance estimation: LedoitWolf vs OAS and max-likelihood

Normal, Ledoit-Wolf and OAS Linear Discriminant Analysis for classification

Gallery generated by Sphinx-Gallery <https://sphinx-gallery.github.io> _